The article titled "Is Monetary Policy Sufficiently Restrictive?" by James Bullard, President of the Federal Reserve Bank of St. Louis, discusses whether the policy rate is restrictive enough to bring inflation back to the 2% target set by the Federal Open Market Committee (FOMC).

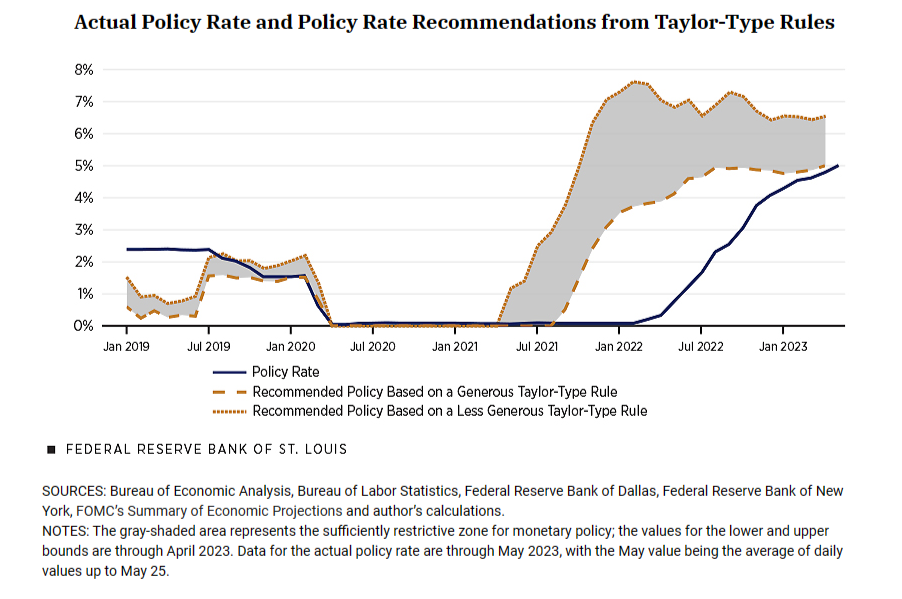

The chart below illustrates a range between the generous Taylor-type rule (5%) and the less generous Taylor-type rule (6.5%). The current Federal funds rate stands at 5.25%. Prior to the pandemic, the Federal Reserve's monetary policy was in line with Taylor's rule. However, the Federal Reserve began to increase the Federal funds rate later than it should have, initiating the rise only in early 2022 instead of early 2021 or at least late summer 2021. This indicates that the Federal Reserve was lagging by approximately 6 to 9 months.

Despite this delay, the Federal Reserve has been rapidly increasing the rate and has finally caught up with the range recommended by the Taylor rules. Nevertheless, the Federal funds rate is still 1.25% lower than the policy recommendation based on the less generous Taylor-type rule. Therefore, if inflation rates rise again or persist, the Federal Reserve has the option to increase the Federal funds rate by another 0.5%. Alternatively, if it chooses not to raise the rates, it can maintain the current Federal funds rate for an extended period.

Source: Is Monetary Policy Sufficiently Restrictive? | St. Louis Fed (stlouisfed.org)

Key points from the article:

1. Since mid-2021, inflation has been running above the 2% target. To counter this, the FOMC began a series of increases to the federal funds rate (the policy rate) in March 2022, aiming to make monetary policy "sufficiently restrictive" to return inflation to 2% over time.

2. The current range for the federal funds rate is 5%-5.25% following the increase at the May FOMC meeting.

3. The article discusses the use of monetary policy rules, specifically the "Taylor rule," to determine if the policy rate is sufficiently restrictive. These rules provide explicit recommendations for the level of the policy rate given macroeconomic conditions.

4. The author presents an assessment of a "sufficiently restrictive zone" for the policy rate using two versions of the Taylor-type rule, one with generous assumptions and one with less generous assumptions. The area between the lower and upper bounds of these rules can be considered the "sufficiently restrictive zone."

5. According to this analysis, monetary policy was about right before the COVID-19 pandemic, as the actual policy rate was within the zone. However, the policy rate was below the zone in 2022, suggesting that monetary policy was behind the curve at that point. But since the FOMC has raised the policy rate aggressively during 2022 and into 2023, monetary policy is now at the low end of what is arguably sufficiently restrictive given current macroeconomic conditions.

6. Both headline and core PCE inflation have declined from their peaks in 2022, but they remain too high. Market-based inflation expectations have returned to levels consistent with the 2% inflation target, which is an encouraging sign that inflation will decline to 2%. However, continued vigilance is required.

No comments:

Post a Comment