library(ggplot2)

library(tseries);library(timeseries);library(xts);library(forecast)

library (quantmod)

library(psych)

library(plotly) #install.package(plotly)

#Service-Providing Industries (SRVPRD)

#USGOOD - All Employees: Goods-Producing Industries

#Private Service-Providing (CES0800000001)

#Mining and Logging: Oil and Gas Extraction (CES1021100001)

#Construction (USCONS)

#Manufacturing (MANEMP)

#Durable Goods (DMANEMP)

#Nondurable goods (NDMANEMP)

#Trade, Transportation and Utilities (USTPU)

#Wholesale Trade (USWTRADE)

#Transportation and Warehousing (CES4300000001)

#Retail Trade (USTRADE)

#Utilities (CES4422000001)

#Information Services (USINFO)

#Financial Activities (USFIRE)

#Professional and Business Services (USPBS)

#Education and Health Services (USEHS)

#Leisure and Hospitality (USLAH)

#Other Services (USSERV)

#Government (USGOVT)

getSymbols(c('PAYEMS','USGOOD','SRVPRD','CES0800000001','CES1021100001','USCONS','MANEMP',

'DMANEMP','NDMANEMP','USTPU','USWTRADE','USTRADE','CES4300000001','CES4422000001',

'USINFO','USFIRE','USPBS','USEHS','USLAH','USSERV','USGOVT'), from="1990-01-01",src='FRED')

EMP<-merge (PAYEMS,USGOOD,SRVPRD,CES0800000001,CES1021100001,USCONS,MANEMP,

DMANEMP,NDMANEMP,USTPU,USWTRADE,USTRADE,CES4300000001,CES4422000001,

USINFO,USFIRE,USPBS,USEHS,USLAH,USSERV,USGOVT)

names(EMP)<-c('PAYEMS','USGOOD','SRVPRD','CES0800000001','CES1021100001',

'USCONS','MANEMP','DMANEMP','NDMANEMP','USTPU',

'USWTRADE','USTRADE','CES4300000001','CES4422000001',

'USINFO','USFIRE','USPBS','USEHS','USLAH',

'USSERV','USGOVT')

# % in Total Nonfarm

PER_Good=USGOOD/PAYEMS*100

PER_Service=SRVPRD/PAYEMS*100

PER_CES0800000001=CES0800000001/PAYEMS*100

PER_CES1021100001=CES1021100001/PAYEMS*100

PER_USCONS=USCONS/PAYEMS*100

PER_MANEMP=MANEMP/PAYEMS*100

PER_DMANEMP=DMANEMP/MANEMP*100

PER_NDMANEMP=NDMANEMP/MANEMP*100

PER_USTPU=USTPU/PAYEMS*100

PER_USTRADE=USTRADE/PAYEMS*100

PER_USINFO=USINFO/PAYEMS*100

PER_USPBS=USPBS/PAYEMS*100

PER_USEHS=USEHS/PAYEMS*100

PER_USWTRADE=USWTRADE/PAYEMS*100

PER_USFIRE=USFIRE/PAYEMS*100

PER_USLAH=USLAH/PAYEMS*100

PER_USSERV=USSERV/PAYEMS*100

PER_USGOVT=USGOVT/PAYEMS*100

plot(PER_CES1021100001)

PER_USPBS

summary(PER_USCONS)

hist(PER_USCONS)

# Chart for Total Nonfarm

myColors <- c("red", "darkblue")

plot(x = EMP_PER, xlab = "Year", ylab = "% in Total Nonfarm",

main = "% in Total Nonfarm Employment",col=myColors, screens = 1)

legend(x = "bottom", legend = c('USGOOD','SRVPRD'),

lty = 1, col=myColors)

plot(x = EMP_MAN, xlab = "Year", ylab = "% in Manufacturing",

main = "% in Total Manufacturing Employment",col=myColors, screens = 1)

legend(x = "bottom", legend = c('Durable','NonDurable'),

lty = 1, col=myColors)

write.table(EMP, file='EMP.xls')

myColors <- c("red", "darkblue","brown","yellow","darkred","blue","pink","green","violet","black")

plot(x = last(EMP, "30 years"), xlab = "Year", ylab = "Index",

main = "CPI", col=myColors, screens = 1)

legend(x = "topleft", legend = c('PAYEMS','USGOOD','SRVPRD','CES0800000001','CES1021100001',

'USCONS','MANEMP','DMANEMP','NDMANEMP','USTPU',

'USWTRADE','USTRADE','CES4300000001','CES4422000001',

'USINFO','USFIRE','USPBS','USEHS','USLAH',

'USSERV','USGOVT'),

lty = 1, col=myColors)

Diff_EMP <- (EMP/lag(EMP)-1)

Diff_EMP[1,] <- 0

Diff_EMP12<-diff(EMP,lag =12)

write.table(Diff_EMP, file='Diff_EMP.xls')

tail(Diff_EMP12)

# Retail Trade

par(mfrow=c(3,1))

plot(USTRADE, main="Retail Trade", col="black")

barplot(Diff_EMP12$USTRADE, main="Changes from previous year ", col="red")

barplot(annualReturn(USTRADE), main=" Annual Changes ", col="blue")

# Financial Activities

par(mfrow=c(3,1))

plot(USFIRE, main="Financial Activities", col="black")

barplot(Diff_EMP12$USFIRE, main="Changes from previous year ", col="red")

barplot(annualReturn(USFIRE), main=" Annual Changes ", col="blue")

# Professional and Business Services

par(mfrow=c(3,1))

plot(USPBS, main="Professional and Business Services", col="black")

barplot(Diff_EMP12$USPBS, main="Changes from previous year ", col="red")

barplot(annualReturn(USPBS), main=" Annual Changes ", col="blue")

# Education and Health Services

par(mfrow=c(3,1))

plot(USEHS, main="Education and Health Services", col="black")

barplot(Diff_EMP12$USEHS, main="Changes from previous year ", col="red")

barplot(annualReturn(USEHS), main=" Annual Changes ", col="blue")

# Leisure and Hospitality

par(mfrow=c(3,1))

plot(USLAH, main="Leisure and Hospitality", col="black")

barplot(Diff_EMP12$USLAH, main="Changes from previous year ", col="red")

barplot(annualReturn(USLAH), main=" Annual Changes ", col="blue")

# Other Services

par(mfrow=c(3,1))

plot(USSERV, main="Other Services", col="black")

barplot(Diff_EMP12$USSERV, main="Changes from previous year ", col="red")

barplot(annualReturn(USSERV), main=" Annual Changes ", col="blue")

# US Government

par(mfrow=c(3,1))

plot(USGOVT, main="Government", col="black")

barplot(Diff_EMP12$USGOVT, main="Changes from previous year ", col="red")

barplot(annualReturn(USGOVT), main=" Annual Changes ", col="blue")

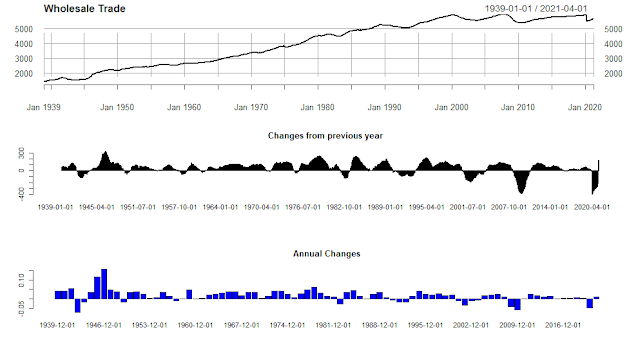

# Wholesale Trade

par(mfrow=c(3,1))

plot(USWTRADE, main="Wholesale Trade", col="black")

barplot(Diff_EMP12$USWTRADE, main="Changes from previous year ", col="red")

barplot(annualReturn(USWTRADE), main=" Annual Changes ", col="blue")

# Mining and Logging: Oil and Gas Extraction

par(mfrow=c(3,1))

plot(CES1021100001, main="Mining and Logging: Oil and Gas Extraction", col="black")

barplot(Diff_EMP12$CES1021100001, main="Changes from previous year ", col="red")

barplot(annualReturn(CES1021100001), main=" Annual Changes ", col="blue")