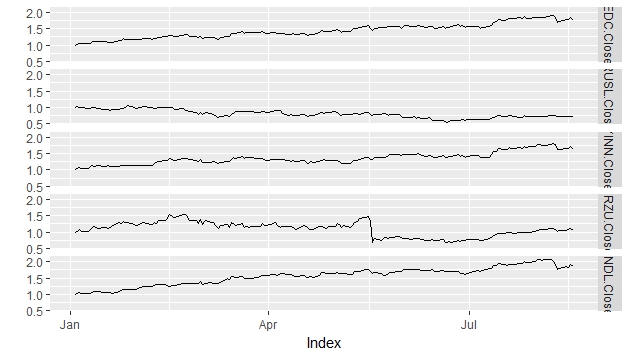

The emerging stock markets:

EDC (Direxion Daily MSCI Em Mkts Bull 3X ETF (EDC))

RUSL (Direxion Daily Russia Bull 3X Shares(RUSL))

YINN (Direxion Daily FTSE China Bull 3X ETF (YINN))

BRZU (Direxion Daily MSCI Brazil Bull 3X ETF (BRZU))

INDL (Direxion Daily MSCI India Bull 3X Shares )

If you have invested $1.00 at the beginning of year, then the returns would be following: India would the highest yield among emerging countries.

EDC.Close RUSL.Close YINN.Close BRZU.Close INDL.Close

2017-08-10 1.703108 0.7183414 1.611931 1.011147 1.752255

2017-08-11 1.720110 0.7172208 1.619628 1.040188 1.789659

2017-08-14 1.772395 0.7162869 1.661963 1.044881 1.859186

2017-08-15 1.775503 0.7209563 1.651058 1.077442 1.839824

2017-08-16 1.831810 0.7293612 1.724182 1.117630 1.914631

2017-08-17 1.758318 0.7259993 1.622835 1.058082 1.853685